The cashflow statement, explained

By Benoit Sarrade

/ June 16, 2022

Cash is king. You probably heard that one before, and for companies, it does hold some truth. Cash is the...

Read More

We use the ROCE as one the winning criteria, in many of our business simulation games, as a measure of business success.

Success is not an easy term to define, as we often realize with participants of our business games. The same applies in real life – is your organization successful? If so, what did you base this conclusion on? Is success a high sales turnover? Is it linked to your volumes? Is it employee morale or sustainability?

Rather, we believe at MEGA Learning that an organization’s success can be assessed against a wider range of criteria, among which the Return on Capital Employed (ROCE) holds a special place.

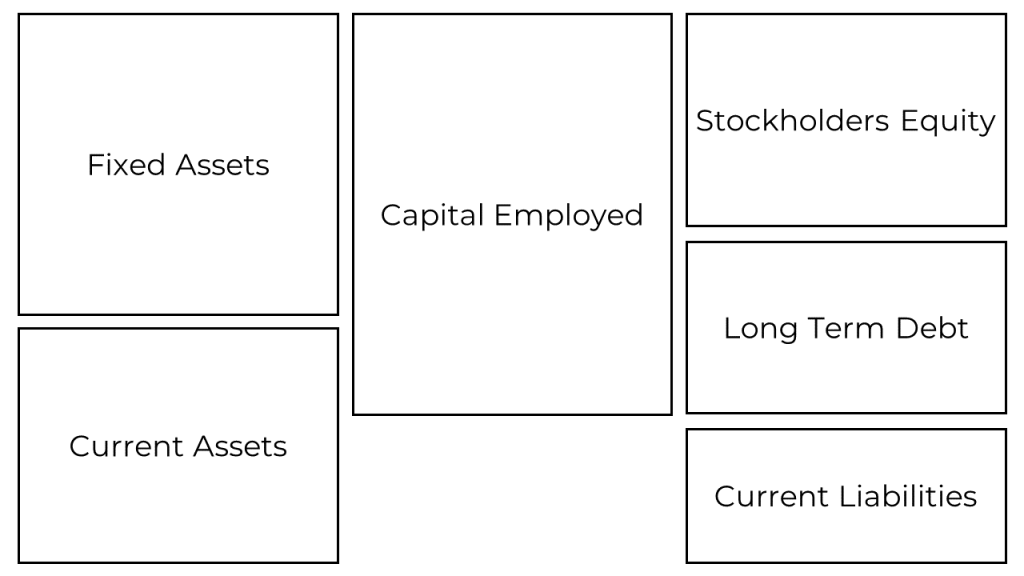

Before we dive into the ins and outs of the Return on Capital Employed, we need a refresher of what Capital Employed stands for.

Simply put, it is the total amount of capital that a company has put in to generate profits – it is a snapshot of how a company is investing its money. It can be calculated by deducting short-term financial obligations (current liabilities, e.g. accounts payable, short-term debts, dividends, etc.) from the total assets of the company (anything the company owns with the expectation to generate profit), for example.

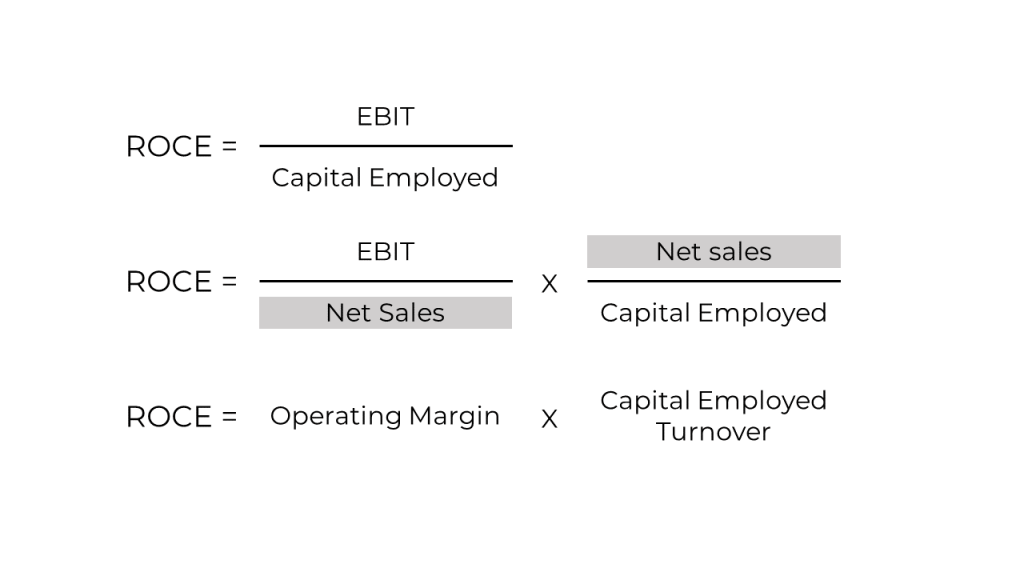

The Return on Capital Employed is calculated by comparing the profits of the company with its capital employed.

Mathematically, this means dividing the EBIT by the amount of capital employed. The ROCE therefore indicates the efficiency and profitability of the company’s capital investment.

If we break down the ROCE (as in the DuPont Analysis) we can gain a much better understanding of where movements in ROCE are coming from.

The ROCE formula allows us to identify two clear elements:

1) on the left-hand side is the operating margin – which measures how much profit a company generates from each euro of sales (in %) and relates to a company’s prices, costs, expenses, and product mix.

2) on the right-hand side is the capital employed turnover – which measures how much your organization is selling compared to the amount of capital that has been put in, which relates to your inventory, receivables, payables and fixed asset.

Simply put, the operating margin (left element) can be increased by reducing the cost of goods sold or increasing prices, to basically generate more profit per unit sold. The CET (right element) can be increased by selling larger volumes for the same amount of capital put into generating sales – or by selling the same amount with less capital invested.

A jewelry shop is positioned to sell products with a high value and will be expecting high margins on each of the pieces they sell.

Let’s say the shop has a 30% operating margin – i.e. generates €0.3 worth of profit per €1 of sales – and has a Capital Employed Turnover of 0.4 – i.e. they don’t sell big volumes and have high levels of capital employed because of the value of their inventory, the hype location of the shop, compared to their sales.

The ROCE of this jewelry shop is therefore 0.3*0.4 = 12% – meaning every euro invested in the shop generates €0.12 of profit.

Let’s look at the case of a supermarket now. Supermarkets have a low operating margin per product sold, which means they need to make sure their Capital Employed Turnover is very high – i.e. they need to sell their stocks as soon as possible and sell big volumes. Besides, the investment in building capacity is very low.

Fresh food, for example, will stay on display for maximum 3 days, meaning the turnover is very high. If the supermarket has an operating margin of 5% – meaning they make €0.05 per €1 of sales – they can reach the same level of ROCE as the jewelry shop (12%) by having a Capital Employed Turnover of 2.4 – by increasing sales and reducing capital employed.

As another illustration, one could take the example of a French high-end restaurant and a Chinese lunch canteen.

They could both have the same level of ROCE but with a different mix of operating margin and capital employed turnover: the French restaurant is priced very high and has a limited number of seats per service. There will be probably one reservation per table per service: if people come to eat, the restaurant will try to increase their consumption, by selling aperitives, expensive wines, desert, coffee and other high-margin products.

The operating margin is probably very high (e.g. 40% on these extras) but the overall volume of sales is low compared to how much capital is employed (0.8) – the restaurant probably has a lot of expensive decoration, is probably located in a upscale area, buying expensive ingredients, etc. The ROCE would be 32%.

For the Chinese canteen to reach the same results in terms of ROCE, they will not be able to count on operating margin, as prices are way lower – e.g. a 10% operating margin -, but their Capital Employed Turnover can be increased substantially by increasing the number of clients/reservation per table per service , and therefore sales, while decreasing Capital Employed (e.g. a less upscale location, lower-valued total assets, etc.). If this restaurant wants a 32% ROCE, they will need a CET of 3.2 !

What is key is to understand which business you are in.

As we have seen with the jewelry store vs. the supermarket, or in the case of a Chinese canteen vs. a French restaurant, similar levels of generated profit per €1 employed can be achieved in substantially different ways.

Considering the ROCE as a sign of profitability and contributing to company success in our business simulations, we seek to show participants that there is not one way to do business, and that success is not pre-destined by the nature of your product.

Our intuition might lead us to think the jewelry shop or the French restaurant are necessarily more profitable than their cheaper counterparts, yet the fact that the supermarket and the Chinese canteen are in control of the turnover of their capital employed makes them just as successful from a profitability perspective.

This is why our business simulation games introduce a multi-product portfolio, with sensitively different customer profiles and cost sensitivities.

We invite our participants to reach for profitability, be it as the manager of a high-end, luxury car business line, or monitoring a large-scale, low-cost car manufacturing facility.

We also invite them to look at less obvious products, neither luxury nor lower-end, so they learn to find a balance between their operating margin – by making decisions on price, quantities, marketing/engineering expenses – and their capital employed turnover – by paying attention to their facility investment, their inventory and the horizon of their payables/receivables, among others.

Individually or as a team, participants will need to make decisions based on the natural sensitivities of the market, in a highly competitive environment.

If you would like to know more about what it looks like, get in touch!